The market in the United Kingdom has been flat over the last week, but it has risen 11% in the past 12 months with earnings expected to grow by 14% per annum over the next few years. In this environment, identifying growth companies with high insider ownership can be particularly advantageous as it often indicates strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

|

Name |

Insider Ownership |

Earnings Growth |

|

Filtronic (AIM:FTC) |

28.6% |

33.5% |

|

Integrated Diagnostics Holdings (LSE:IDHC) |

27.6% |

23.7% |

|

Helios Underwriting (AIM:HUW) |

23.9% |

14.7% |

|

Foresight Group Holdings (LSE:FSG) |

31.9% |

27.9% |

|

LSL Property Services (LSE:LSL) |

10.8% |

33.3% |

|

Belluscura (AIM:BELL) |

36.1% |

113.4% |

|

B90 Holdings (AIM:B90) |

24.4% |

142.7% |

|

Velocity Composites (AIM:VEL) |

27.6% |

188.7% |

|

Judges Scientific (AIM:JDG) |

11.9% |

27.5% |

|

Gulf Keystone Petroleum (LSE:GKP) |

12.1% |

80.6% |

We’re going to check out a few of the best picks from our screener tool.

Simply Wall St Growth Rating: ★★★★☆☆

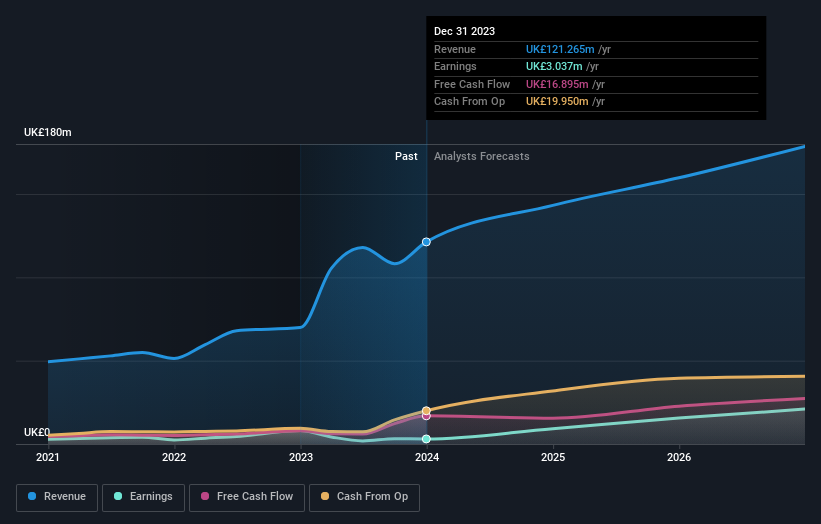

Overview: Franchise Brands plc, with a market cap of £357.53 million, operates through its subsidiaries in franchising and related activities across the United Kingdom, North America, and Europe.

Operations: The company’s revenue segments include Azura (£0.75 million), Pirtek (£41.95 million), B2C Division (£6.11 million), Water & Waste (£48.88 million), and Filta International (£27.12 million).

Insider Ownership: 26.6%

Earnings Growth Forecast: 40.7% p.a.

Franchise Brands, a growth company with high insider ownership, is forecast to see significant annual earnings growth of 40.7%, outpacing the UK market’s 14.3%. Despite trading at 48.5% below its fair value estimate and experiencing recent executive changes, insiders have been buying more shares than selling in the past three months. However, profit margins have declined from 11.6% to 2.5%, and large one-off items have impacted financial results recently.

Simply Wall St Growth Rating: ★★★★☆☆

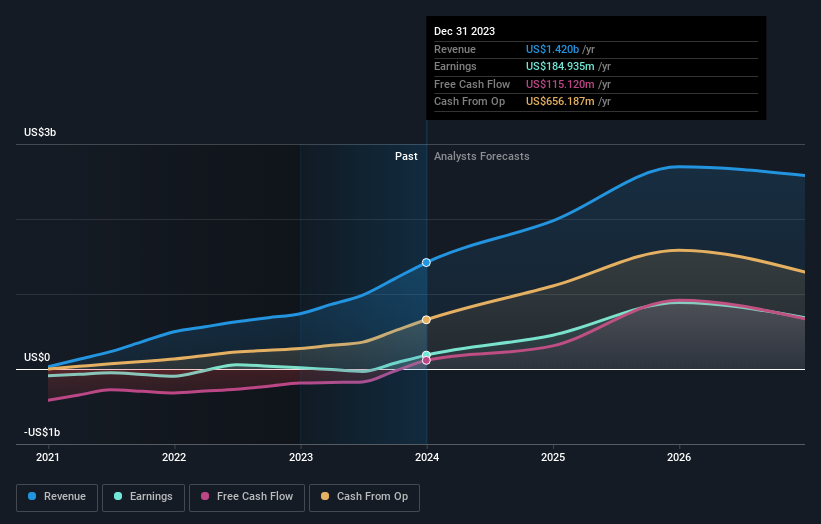

Overview: Energean plc is involved in the exploration, production, and development of oil and gas, with a market cap of £1.78 billion.

Operations: Revenue from oil and gas exploration and production amounts to $1.42 billion.

Insider Ownership: 10.6%

Earnings Growth Forecast: 14.6% p.a.

Energean, with substantial insider ownership, is forecast to grow earnings by 14.56% annually, outpacing the UK market’s 14.3%. Despite high debt levels and recent shareholder dilution, it trades at 53% below fair value estimates. Recent business expansions include the Cassiopea field in Italy and the Katlan project in Israel. Insiders have shown confidence by buying more shares than selling over the past three months, although not in large volumes.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC, with a market cap of £1.74 billion, offers banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan through its subsidiaries.

Operations: The company generates revenue from various segments, including GEL 2.13 billion from segment adjustments and GEL 236.42 million from its operations in Uzbekistan.

Insider Ownership: 17.6%

Earnings Growth Forecast: 15.3% p.a.

TBC Bank Group, with significant insider ownership, is forecast to grow earnings by 15.3% annually, surpassing the UK market’s 14.3%. Despite a low allowance for bad loans and recent shareholder dilution, it trades at 46.1% below fair value estimates and offers good relative value compared to peers. Recent half-year results show net income growth from GEL 537.46 million to GEL 617.4 million year-over-year, reflecting strong financial performance amidst an unstable dividend track record.

Next Steps

Interested In Other Possibilities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include AIM:FRAN LSE:ENOG and LSE:TBCG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com